UK Snap Election 2017. Questions Arising. Hard or Soft Brexit.

Every time a politician says that an election is not a game, there is a clear risk that democracy takes a step back. So on April 8, when Theresa May called a snap UK election for June 8, and said that it was not a game, one should be concerned.

But this is not the reason for this article. I offer no answers, only questions. The situation since the June 23, 2016 referendum has been pure confusion. Nobody on either side of the Leave/Remain divide has any idea how the Brexit process will unfold. The government, charged with managing the divorce, appears not to have a definitive plan, how could it, but has additionally been confounded by internal rifts and special interests. The only mercy, if it can be interpreted as such, is the lack of a credible opposition to challenge its exit … plan.

Why did the PM call a snap election when she strenuously said she would not? Is it an opportunistic tactic to take advantage of Labour’s disarray? Is it that the PM seeks a strong mandate since, as Nicola Sturgeon pointed out, Theresa May is unelected? Or is it to nullify the Cameron manifesto, upon which the 2015 general election was won?

What are the implications for Brexit? Could a stronger Tory majority lead to a softer or more flexible negotiating stance? This seems a bit hopeful as the hardliners are Tories. Is a stronger mandate for the party to imply an endorsement of the PM?

What could upset the widely expected Tory majority? The epic failure of the Lib Dems in the last election followed by the significant rebound they achieved, albeit in one constituency, Richmond Park, shows how volatile the voter sentiment has become. Could a resurgent Lib Dem vote spoil the calculus for a Tory rout of Labour? The Lib Dems were punished for being too moderate a part of the coalition with a hard line Tory government. Could voters seek moderation and vote for the Lib Dems in the coming election?

Could the election become a proxy second referendum on EU membership and if so, how would the votes fall? This is particularly complicated. Is there sufficient ‘buyers’ remorse’ in the country to reanimate the debate? Since the referendum, more new information about the cost and consequences of Brexit have come to light and this could trigger a review of voters’ positions which could result in some surprising results. Any anti Brexit majority constituencies represented by pro Brexit MPs will be interesting battlegrounds.

If indeed a larger Tory majority and a strong mandate for the PM provided the flexibility in negotiating Brexit then clearly this would be positive for the economy. If, however, the election is hijacked by the Eurosceptics then the implications would be quite different.

What if there was a swing to the Lib Dems, which are seen as more moderate and less Eurosceptic? A weaker Tory majority with the Lib Dems in second could be a more moderate combination. Resurgent Labour would ordinarily be less Eurosceptic but the partisan politics could complicate negotiations and would make for a messy Brexit.

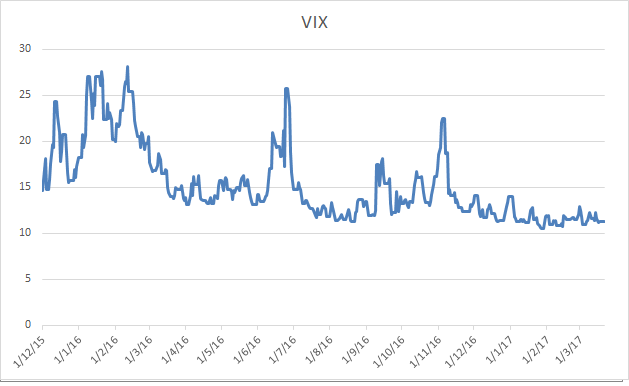

Since June 2016, there has been a persistent natural strength to the UK economy which as yet has not had to contend with the reality of Brexit, only the inevitability of it. And yet, sterling remains some 14% below pre referendum levels. It had been in a rising trend just before the referendum, and was on a rising trend since October 2016, after the initial shock. The shock of a snap election has lifted sterling as the market interprets it as a step towards reducing uncertainty, since the election result, at least for now, seems a foregone conclusion. It may not be, but we will have to see how the next two months unfolds. Unless there are negative shocks, sterling should be on a recovery trend to 1.35. Weak sterling has been responsible for rising UK stocks, so strong sterling will likely reverse or stall the rally. With a stable underlying economy, this is likely a buying opportunity, however, we will need sterling to achieve that level and assess the impact on equities. It is too early to buy UK equities.

Weak sterling has only been partly responsible for the strength of the UK economy. The UK has been faster to clean up its financial and banking industry and unclog the plumbing of credit than the continent and this has paid dividends. Policy in the immediate aftermath of the 2008 crisis was even handed and well executed. The right balance between austerity and fiscal stimulus was found. The economy is therefore more efficient and resilient than its continental counterparts, with the exception perhaps of Germany. In the negotiation and implementation of Brexit, a less militant deal would see UK economic strength continue.

Will the May government with a stronger mandate be more or less militant?

How will French, German and eventually Italian elections unfold? Will the rise of Eurosceptics make Brussels more or less militant?

Economic growth seems at last to be picking up in Europe. Will a stronger European economy encourage more conciliatory tones from both sides?

There is another less comforting interpretation: That Theresa May’s calling of a snap election has nothing to do with Brexit or a strong mandate, but is an opportunistic power grab. If this is so, what can we infer? That May expects the Brexit negotiations to be fraught and sufficiently damaging to party unity and popularity. An election at this point prolongs Tory control for 2 extra years.